What is options Delta and how does it affect price?

The option's delta is the rate of change of the price of the option with respect to its underlying security's price. The delta of an option ranges in value from 0 to 1 for calls (0 to -1 for puts) and reflects the increase or decrease in the price of the option in response to a 1 point movement of the underlying asset price.

How to calculate Delta options?

- Delta = ($46.80 - $45.00) / ($523 - $520)

- Delta = ($1.80) / ($3)

- Delta = +0.6

What is Delta in options trading?

Specifically, delta is a measure of how sensitive the price of the option is relative to changes in the price of the underlying security. Common examples of derivatives for which delta would be calculated are call and put options.

What does Delta options mean?

Options delta is one of the most important factors in making up an options contract. It is a member of the Greeks. Delta measures the rate of change in an options price per $1 move. Example: if an option contract has a delta of $0.35 and the price of the stock rises by $1 then the options contract would increase by $0.35.

See more

What is options delta price?

Delta measures the degree to which an option is exposed to shifts in the price of the underlying asset (i.e., a stock) or commodity (i.e., a futures contract). Values range from 1.0 to –1.0 (or 100 to –100, depending on the convention employed).

What is delta of a stock option?

Delta is the theoretical estimate of how much an option's value may change given a $1 move UP or DOWN in the underlying security. The Delta values range from -1 to +1, with 0 representing an option where the premium barely moves relative to price changes in the underlying stock.

What is a good delta for options?

Call options have a positive Delta that can range from 0.00 to 1.00. At-the-money options usually have a Delta near 0.50.

How is option delta price calculated?

The formula for delta can be derived by dividing the change in the value of the option by the change in the value of its underlying stock. Important: Delta is used to measure the theoretical change in the value of option price given a change in the price of the underlying security.

Is high delta good for options?

Delta is positive for call options and negative for put options. That is because a rise in price of the stock is positive for call options but negative for put options. A positive delta means that you are long on the market and a negative delta means that you are short on the market.

How do you read options delta?

Delta is the amount an option price is expected to move based on a $1 change in the underlying stock. Calls have positive delta, between 0 and 1. That means if the stock price goes up and no other pricing variables change, the price for the call will go up.

What is a good delta to theta ratio?

Basically, for a non-directional trader capitalizing on theta decay, you want to try to target a 0.5 delta-to-theta ratio. Keep delta at 50% or less of your theta, and you should be good. This ratio may not always be possible when the price moves all around in the middle of a trade. It also depends on the underlying.

What is a 30 delta option?

If your long call is showing a delta of . 30, some traders may think of this as having approximately a 30% probability of being in the money. This can be used as a risk management tool.

What is a 20 delta option?

For example, if the option has a delta of 20 it suggests it has a 20% chance of finishing in-the-money. A delta of 50 suggests it has a 50-50 chance of finishing in-the-money. If an options delta is less than 50 it is said to be out of the-money. If the delta is greater than 50 the option is said to be in-the-money.

Can option delta be higher than 1?

Call Option Delta A call option's value increases when the underlying price goes up. Therefore, it makes sense that call delta is always a non-negative number. At the same time, a call option's value can't grow faster than underlying price. As a result, call delta can never be greater than 1.

Are delta options accurate?

For example, an out-of-the-money call option with a 0.20 delta has roughly a 20% chance of being in-the-money at expiration, whereas a deep-in-the-money call option with a 0.95 delta has a roughly 95% chance of being in-the-money at expiration.

How does option delta change with price?

First, delta represents the amount that an option's price will change for every $1 move in the underlying stock. For example, a delta of 0.6 means that for every $1 the underlying stock increases/decreases, the option will increase/decrease by $0.60.

What is a 30 delta option?

If your long call is showing a delta of . 30, some traders may think of this as having approximately a 30% probability of being in the money. This can be used as a risk management tool.

What is delta and theta in options?

Key Takeaways. An option's "Greeks" describes its various risk parameters. For instance, delta is a measure of the change in an option's price or premium resulting from a change in the underlying asset, while theta measures its price decay as time passes.

Can the delta of an option be greater than 1?

Call Option Delta Therefore, it makes sense that call delta is always a non-negative number. At the same time, a call option's value can't grow faster than underlying price. As a result, call delta can never be greater than 1. Call delta value range is from zero to positive one.

Does delta mean difference?

Difference is the most common meaning of the uppercase delta. It is simply the difference, or change, in a certain quantity. When we say delta y, for example, we mean the change in y or how much y changes.

Call Option Deltas vs. Put Option Deltas

Call Option Price vs. Stock Price Changes

So, you know the basics of what delta represents, but now it’s time to learn about the differences between call and put deltas. As you may have noticed in the table from the last section, the call deltas are positive, and the put deltas are negative. More specifically:

Put Option Price vs. Stock Price Changes

As an illustration, we analyzed the price changes of a call option traded on SPY. Here are the specifics:

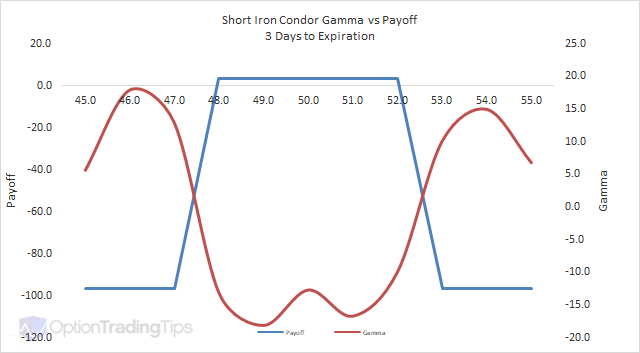

Using Delta to Measure Directional Risk

In this example, we’ll visualize the price changes of the March 200 put on SPY.

Visualizing Call Option Price Sensitivity

Now, it’s time to learn about how an option’s delta value represents its price sensitivity relative to movements in the stock price.

Visualizing Put Option Price Sensitivity

To visualize the price changes of SPY call options with different deltas, we analyzed three separate call options with deltas of +0.25, +0.50, and +0.75, respectively. When examining this visual, notice how each option’s delta translates to its degree of price sensitivity:

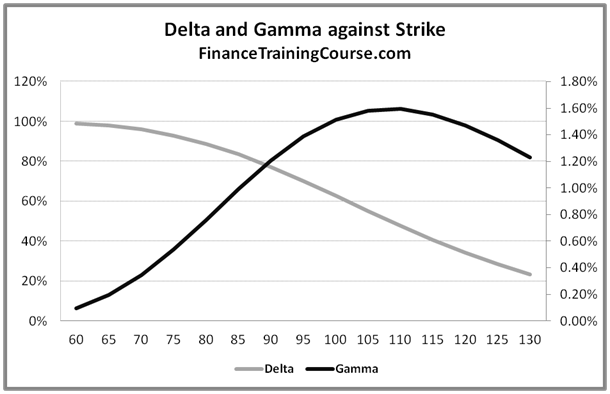

Option Strike Price vs. Delta

To analyze put option price sensitivity based on the option’s delta, we’ll use the same stock, time period, and expiration cycle as before. However, we’ll analyze three separate SPY put options with deltas of -0.25, -0.50, and -0.75, respectively.