Full Answer

Could hp's stock see further downside at $16?

Despite having declined over 20% since the beginning of this year, at the current price of $16 per share, we believe HP Inc. (NYSE: HPQ) could see further downside. Why is that? The key is HPQ’s stock is down nearly the same amount since the start of this year, as it has been since the start of 2019, a little over a year ago.

Why has HPQ's stock dropped so much?

This drop in HPQ’s stock has largely been due to the 41% slump seen in HPQ’s PE multiple from around 13x at the end of 2018 to 10x at the end of 2019. HPQ’s PE multiple is further down to below 8x, given the volatility of the current situation, and the stock is down to levels last seen at the start of 2017.

What does hp’S P/S ratio look like right now?

Right now, HP has a P/S ratio of 0.43. This is much lower than the S&P 500 average, which comes in at 2.93 right now. Also, as we can see in the chart below, this is somewhat below the highs for this stock in particular over the past few years.

Is HP Inc's most profitable part of the company struggling?

With the most profitable part of HP struggling, it's not surprising that the market punished the stock on Thursday. This article represents the opinion of the writer, who may disagree with the “official” recommendation position of a Motley Fool premium advisory service.

Is HP stock a good buy?

HP is a good long-term investment, but it will be tough for its shares to re-rate in the near-term given expectations of top line contraction starting in fiscal 2023.

Why is HP a good stock?

HP's Q2 earnings beat Wall Street's expectations. Its top-line growth is decelerating, but its EPS growth remains robust. Its shareholder-friendly measures and low valuation make it a good safe haven stock to own in this volatile market.

Is HP a good long-term investment?

The long-term earnings per share growth rate is estimated at 6%. Hewlett Packard has an impressive earnings surprise history. The company outpaced estimates in all the trailing four quarters, delivering an average earnings surprise of 10.7%.

Why is Buffett buying HP?

HP has bought back over 25% of its stock since October 2019, the end of its fiscal 2019. Buffett likes companies that can comfortably fund big buybacks because the purchases increase Berkshire's percentage ownership of them.

Did Warren Buffett buy HP?

Warren Buffett's Berkshire Hathaway Bought HP Stock.

Which HP stock did Buffett buy?

Buffett has stepped up to the tech batter's box again — according to the Wall Street Journal, he is now the proud owner of an 11% stake in PC Maker HP.

Is HP undervalued?

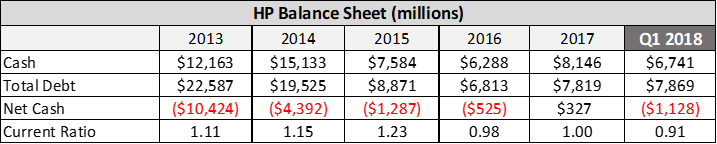

Conclusion. HP Inc., shows qualities of an undervalued stock, with regular profits and adequate capitalization. Our valuation model shows that the company's cash flows are mispriced even in a scenario with limited growth.

Is HP a Buy Sell or Hold?

HP has received a consensus rating of Hold. The company's average rating score is 1.92, and is based on 2 buy ratings, 7 hold ratings, and 3 sell ratings.

Is HP growing?

HP is also cash rich. The company has generated cash flow growth of 11.6%, and is expected to report cash flow expansion of 34.4% in 2022. Investors should take the time to consider HPQ for their portfolios due to its solid Zacks Rank rating, notable growth metrics, and impressive Growth and VGM Style Scores.

Does HP have a moat?

HP has only one product line at most with a wide moat against challengers—and even that line, printers, is slipping as people print less because of the proliferation of mobile devices.

How much did Warren Buffet pay for HP?

Warren Buffett made about $650 million on HP after stake was revealed. Shares of HP soared on Thursday after Warren Buffett's Berkshire Hathaway revealed it owns 121 million shares of the PC and printer maker. HP's stock rose 15%, boosting the value of Berkshire's stake by about $650 million to $4.85 billion.

What happened

Shares of PC and printers maker HP ( HPQ -0.60% ) -- the artist formerly known as Hewlett-Packard -- are down 12.4% as of 11:05 a.m. EDT despite last night's report of a big earnings beat.

So what

I don't think it's that "sales miss," however, that's dragging HP stock down this morning -- certainly not if the company managed to beat on earnings so soundly despite the lower-than-expected sales.

Now what

In its guidance yesterday, HP predicted that Q3 earnings will fall somewhere between $0.35 and $0.41 per share on a GAAP basis and range from $0.39 to $0.45 per share on a pro forma basis. All of these numbers, however, fall short of the $0.49-per-share pro forma earnings that Wall Street has been telling investors to expect.

The company was blindsided by weakness in its printing supplies business

Tim writes about technology and consumer goods stocks for The Motley Fool. He's a value investor at heart, doing his best to avoid hyped-up nonsense. Follow him on Twitter: Follow @TMFBargainBin

What happened

Shares of HP ( NYSE:HPQ) slumped on Thursday after the PC and printer company reported its fiscal first-quarter results. HP missed analyst estimates for revenue, with the company blaming unexpected weakness in its high-margin printing supplies business. The stock was down about 16.3% at 12:15 p.m. EST.

So what

HP reported first-quarter revenue of $14.7 billion, up 1.3% year over year but $150 million below the average analyst estimate. Personal systems revenue was up 2.3% to $9.66 billion, while printing revenue was down 0.4% to $5.06 billion.

Now what

HP expects second-quarter non-GAAP EPS between $0.50 and $0.53 and full-year non-GAAP EPS between $2.12 and $2.22. That represents earnings growth of 5% to 10% for the full year.

Investors have priced in short-term strength as if it's going to last for the long haul

James Brumley is former stockbroker with a large Wall Street firm, and a former trading analyst for a small, options-based newsletter. After twenty years of professional experience in and around the market, his approach is one that combines fundamentals, sentiment, and common sense.

1. We're at peak PC

HP, formerly known as Hewlett-Packard, is certainly well positioned to report strong quarterly numbers next month. The analyst community is modeling nearly 16% sales growth -- in line with IDC's and Gartner's calculations -- driving a 72% improvement in profits.

2. Analysts maintain it's overpriced

Investors should not have blind faith in every analyst estimate. It's noteworthy, however, that the analyst community didn't budge its average target price of just under $31 when the stock blasted well past that point five weeks ago.

3. An unusually high valuation

Finally, HP shares are now at valuation levels this stock hasn't seen since 2018. That's when notebook sales and prices were firming up and investors were celebrating a couple of small acquisitions. Neither tailwind would last, quickly deflating the stock's premium valuation.

Bottom line

To be clear, my concern is more about the stock and less about the company. HP may never be a high-growth company again, but to a certain set of investors, it's a rare dividend play from the technology sector.

What happened

Shares of HP ( HPQ -1.85% ) have plunged today, closing down 14%, after smaller rival Xerox ( XRX ) abandoned its hostile takeover attempt. Yesterday evening, Xerox said it was formally withdrawing its tender offer to acquire all of HP's outstanding shares.

So what

Ever since late 2019, Xerox has been trying to acquire HP. Initially, talks were cordial as Xerox negotiated with HP's board, but after multiple spurned offers, the company launched a hostile takeover in the form of a tender offer appealing directly to shareholders. Xerox's offer of $24 per share was the same price that HP's board had rejected.

Now what

"We remain firmly committed to driving value for HP shareholders. HP is a strong company with market leading positions across Personal Systems, Print, and 3D Printing & Digital Manufacturing," HP responded.

Is HP a separate company?

became the new name for the Hewlett-Packard Company, as Hewlett Packard Enterprise Company ( HPE) (its cloud computing business) got spun off in a separate company. The part which is left, HP Inc., is a leading laptop, desktop, and printing manufacturer. HPQ is a company that is strongly focused to generate shareholder value. They returned $9.1 bln to shareholders last year (a staggering 38% of its current market cap), the dividend yields a solid 4.2% and they beat EPS consensus in 17 out of the past 17 quarters. Its business is divided into two segments: personal systems and print.

Does HP print have strong margins?

The HP print division generates stronger margins but is seeing its market stagnating significantly as digital is disrupting the business. Therefore, HP is committed to drive earnings growth via margin expansion rather than revenue growth. I like the initiatives it takes to sell to customers more directly to improve margins. For example, they managed to grow their "Instant Ink" program to >6 million users. This program connects the printer with the user laptop and automatically orders ink when it knows that you are running low. Interestingly, it includes not paying for ink cartridges anymore but paying a monthly fee based on the number of pages you print. This is an interesting model as it leads to monthly fixed payments (recurring revenues) and leads to higher margins as the middleman is removed. Revenues in Instant Ink grew 3x over the past 3 years and customer retention is very high (>90%). HP is sharing market leadership with Canon Inc. ( CAJ) but managed to outperform competitors by far recently. This could be explained by its strong Instant Ink growth and its leadership in 3D printing.

Is HPQ a saturated market?

As I already explained, HPQ is operating in saturated markets. Thus, expected growth rates are low and competition for market share will increase, which leads to lower valuation. This is not only applicable to HPQ but also to its peers. Let's have a look at how HPQ compares to them. Indeed, it is remarkable that all peers are valued cheaply as well. However, I believe HP Inc. provides much more quality with almost no debt, higher margins, and higher growth than on average. Also, the company is market leader in its both segments, which should be rewarded with a premium. Xerox has very poor growth, Dell has a risky balance sheet and a history of negative margins, and Lenovo has razor thin margins. Therefore, I do not believe HPQ should be compared to these poor companies.

What is HPQ stock?

Today at 6:07 AM ET, HP (NYSE:HPQ) stock fell 6.3% to $16.05 in the pre-market session following its results for the second quarter of fiscal 2020 on Wednesday. Notably, the quarter ended on April 30. The technology company reported mixed results in the second quarter. Although the earnings beat analysts’ consensus expectation, the sales missed the estimates. The company’s third-quarter earnings guidance was lower than Wall Street’s estimates.

How much will HP save in 2022?

On top of all that, HP announced last year it planned to slash between 7,000 and 9,000 jobs by the end of 2022 to save $1 billion a year.”. Analysts also expect HP’s revenues to fall by 6.7% YoY (year-over-year) in fiscal 2020 to $54.8 billion. The sales could rise by 0.4% YoY in fiscal 2021 to $55.0 billion.

Is HP stock overbought?

HP stock has a middle Bollinger Band level of $15.69, while its lower Bollinger Band level is $13.61. On Wednesday, the stock closed near its upper Bollinger Band level of $17.12, which suggests that it’s overbought.