That way, any distributions will reduce the shareholder’s stock basis, helping to avoid taxable income. If the first payment is considered additional paid-in capital, then any additional payments to the principal (owner) are considered dividend distribution (or wage) and will be taxable.

Full Answer

What is the accounting for a small stock dividend?

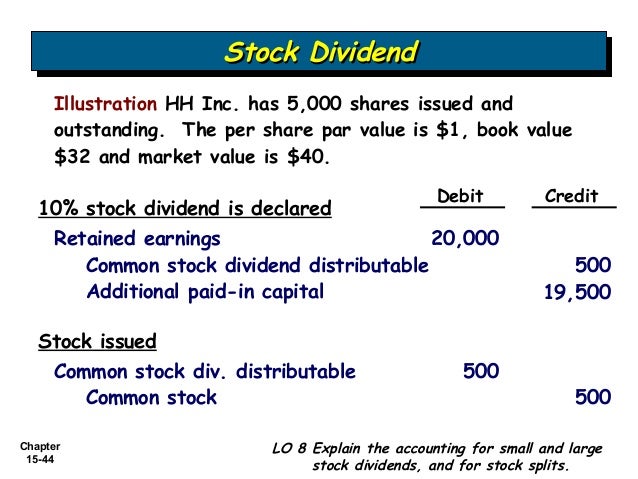

The accounting for a small stock dividend. If the issuance is for a greater proportion of the previously outstanding shares, then treat the transaction as a stock split. When there is a stock dividend, you should transfer from retained earnings to the capital stock and additional paid-in capital accounts an amount equal to the fair value...

What is additional paid-in capital?

Additional paid-in capital is an accounting term used to describe the amount an investor pays above the stock's par value. The par value, which can be for either common or preferred stock, is the value of the stock as stated in the corporate charter.

What happens to the capital stock account when shares are issued?

One effect of this transaction is that the amount of legal capital (the capital stock account) is increased by the par value of the additional shares issued; this amount can no longer be issued to shareholders as a dividend. A stock dividend is never treated as a liability, since it does not reduce assets.

What happens to retained earnings when there is a stock dividend?

When there is a stock dividend, you should transfer from retained earnings to the capital stock and additional paid-in capital accounts an amount equal to the fair value of the additional shares issued. The fair value of the additional shares issued is based on their market value after the dividend is declared.

How does Additional paid in capital affect dividends?

Since cash dividends are deducted from a company's retained earnings, there is no effect on the additional paid-in capital. The amount equivalent to the value of stock dividends is deducted from retained earnings and capitalized to the paid-in capital account.

How do you record a small stock dividend?

How to Account for a Small Stock Dividend. When there is a stock dividend, you should transfer from retained earnings to the capital stock and additional paid-in capital accounts an amount equal to the fair value of the additional shares issued.

What does additional paid in capital mean?

Additional paid-in capital (APIC, or sometimes referred to as capital in excess of par value) is the excess amount paid by an investor over the par value of a stock issue.

What is a small stock dividend?

A stock dividend is considered small if the shares issued are less than 25% of the total value of shares outstanding before the dividend. A journal entry for a small stock dividend transfers the market value of the issued shares from retained earnings to paid-in capital.

Are small stock dividends recorded at market value?

There are two types of stock dividends—small stock dividends and large stock dividends. The key difference is that small dividends are recorded at market value and large dividends are recorded at the stated or par value.

What's the difference between a large stock dividend and a small stock dividend?

When a company issues a stock dividend, it will typically be expressed as a percentage of the total amount of outstanding shares. If the stock dividend is less than 25% of outstanding shares, then it is considered a small stock dividend. If it is greater than 25%, it is considered a large stock dividend.

How do you record additional paid in capital?

Additional paid-in capital is recorded on a company's balance sheet under the stockholders' equity section. The account for the additional paid-in capital is created every time when a company issues new shares to or repurchases its shares from shareholders.

How does Additional paid in capital affect basis?

Paid-in capital does not have an effect on stock basis. The two values are related -- the amount that a company lists as paid-in capital is almost identical to the buyer's basis -- but the terms apply to two different values for two different parties.

What causes additional paid in capital to increase?

How to Increase Additional Paid-In Capital. The recorded amount of additional paid-in capital can only increase when an issuer sells more stock to investors, where the price at which the shares are sold exceeds the par value of the shares.

Does a small stock dividend increase retained earnings?

If a company pays stock dividends, the dividends reduce the company's retained earnings and increase the common stock account. Stock dividends do not result in asset changes to the balance sheet but rather affect only the equity side by reallocating part of the retained earnings to the common stock account.

How do you record stock dividends in journal entry?

The journal entry to record the stock dividend distribution requires a decrease (debit) to Common Stock Dividend Distributable to remove the distributable amount from that account, $1,500, and an increase (credit) to Common Stock for the same par value amount.

Which accounts are ultimately affected by a small stock dividend?

Which accounts are ultimately affected by a small stock dividend? Common Stock, Paid-in Capital in Excess of Par—Common Stock, and Retained Earnings.

What is additional paid in capital?

Additional paid-in capital is an accounting term used to describe the amount an investor pays above the stock's par value. Since cash dividends are deducted from a company's retained earnings, there is no effect on the additional paid-in capital. The amount equivalent to the value of stock dividends is deducted from retained earnings ...

How are dividends paid out?

Dividends can be paid out in different forms—in cash or in-kind in the form of stock. 2 But where does the company get the money for each? Some are debited from a subaccount called the additional paid-in capital. 3 Read on to find out how the company's additional paid-in capital is affected by the issuing of certain dividends.

What is a stock dividend?

A stock dividend results in an issuance equal to or less than 25% of outstanding shares. When a company issues a stock dividend, an amount equivalent to the value of the issued shares is deducted from retained earnings and capitalized to the paid-in capital account. Basically, the common stock and additional paid-in capital sub accounts are ...

Why do companies pay dividends?

Most companies that pay out stock dividends do so if they don't have enough cash reserves to reward their investors. The amount of stock dividends paid out depends on the number ...

What happens when a company sells shares?

When a company agrees to sell shares in an initial public offering (IPO) or a new stock issue, it normally sets the price at the par value. The company may decide to put up a certain amount of shares at a higher price. Whatever the company collects from the sale over and above their par value is put into the company's additional paid-in capital ...

What happens if a company issues a cash dividend?

If a company decides to issue a cash dividend to its shareholders, the funds are deducted from its retained earnings, and there is no effect on the additional paid-in capital.

How do dividends work?

Dividends are a common way for companies to pay back some of their capital to shareholders. 1 Consider it kind of like a reward program for investing in the company. These payouts occur regularly each year, whether that's quarterly, monthly, or semi-annually. Dividends can be paid out in different forms—in cash or in-kind in the form of stock.

What is additional paid in capital?

Key Takeaways. Additional paid-in capital is the difference between the par value of a stock and the price that investors actually pay for it. To be "additional" paid-in capital, an investor must buy the stock directly from the company during its IPO. The additional paid-in capital is usually booked as shareholders' equity on the balance sheet.

When investors buy shares from a given company, that corporation receives and retains the funds as paid-in-

When investors buy shares directly from a given company, that corporation receives and retains the funds as paid-in-capital. But after that time, when investors buy shares in the open market, the generated funds go directly into the pockets of the investors selling off their positions.

What happens to a company's stock price during an IPO?

During its IPO, a firm is entitled to set any price for its stock that it sees fit. Meanwhile, investors may elect to pay any amount above this declared par value of a share price, which generates the additional paid-in capital.

What is paid in capital?

Paid-in capital is the full amount of cash or other assets that shareholders have given a company in exchange for stock. Paid-in capital includes the par value of both common and preferred stock plus any amount paid in excess. Additional paid-in capital, on the other hand, includes only the amount paid in excess of the par value of stock issued during a company's IPO. Both items are included next to one another in the shareholder's equity section of the balance sheet.

Why is paid in capital important?

Additional paid-in capital is a great way for companies to generate cash without having to give any collateral in return. Furthermore, purchasing shares at a company's IPO can be incredibly profitable for some investors.

What is the market value of a stock?

Market Value. Market value is the actual price a financial instrument is worth at any given time. The stock market determines the real value of a stock, which shifts continuously, as shares are bought and sold throughout the trading day.

What is par value?

Simply put, “par” signifies the value a company assigns to stock at the time of its IPO, before there is even a market for the security.

When a stock dividend is declared, should you transfer the earnings to the capital stock?

When there is a stock dividend, you should transfer from retained earnings to the capital stock and additional paid-in capital accounts an amount equal to the fair value of the additional shares issued. The fair value of the additional shares issued is based on their market value after the dividend is declared.

What is a small stock dividend?

Accounting for a small stock dividend. A stock dividend is the issuance by a corporation of its common stock to its common shareholders without any consideration. A dividend of this type is usually issued when a business does not have sufficient cash to spare for a normal dividend, but still wants to give the appearance ...

Is a stock dividend a liability?

One effect of this transaction is that the amount of legal capital (the capital stock account) is increased by the par value of the additional shares issued; this amount can no longer be issued to shareholders as a dividend. A stock dividend is never treated as a liability, since it does not reduce assets.

How are small stock dividends accounted for?

The small stock dividends are accounted for under the US GAAP as follows; When a corporation issues a stock dividend, a distribution of stock transfers part of retained earnings to the contributed capital accounts on the annual balance sheet of the corporation.

When a business does not have enough cash to pay dividends, does it issue a small stock dividend?

Conclusion. When a business does not have enough cash to pay dividends and they issue a small stock dividend, the investors get a return on their investment and the business or corporation does not have to deplete its cash position. Such dividends are also common in mergers and corporate restructuring deals.

What is a small stock dividend?

A small stock dividend is usually common in corporate structures and is defined under the US GAAP (Generally Accepted Accounting Principles) in ASC 505-20 as follows: “A dividend distribution of 25 percent or less outstanding company shares to existing stockholders, is called small stock dividend.”. In other words, a small stock dividend is one ...

What is dividend in stock?

Dividends refer to payments that are made by a company to its shareholders from its accumulated distributable earnings. The dividends will either be in cash or in some kind of consideration (i-e; stocks, shares of a listed company, etc). When a corporation issues a dividend of its common stock to its common shareholders without any consideration, such issuance of dividends is a stock dividend.

Why do companies issue small dividends?

Why does a Company Issue a Small Stock Dividend? A stock dividend is issued by the business when they do not have sufficient cash to give a normal dividend (i-e; cash dividend), but they still want to give the appearance of issuing a dividend payment to its shareholders in their financial statements.

Can ABC use dividend distributable?

If the declared date and issuance date are different, at the date of declaration, ABC can use stock dividend distributable as a temporary account instead of a common stock account and this will be transferred to a common stock account when the stocks are issued. The journal entry for the declaration of small stock dividend will be as follows;

What is additional paid in capital?

What is Additional Paid-in Capital? Additional paid-in capital is the amount paid for share capital above its par value. It is also commonly known as the “contributed capital in excess of “par” or “share premium.”. Essentially, the additional paid-in capital reveals how much money investors paid for the shares above their nominal value.

What is contributed capital?

Contributed capital (also known as the paid-in capital) is the total value of a company’s equity purchased by investors directly from a company. In other words, it indicates the total amount of money that the shareholders paid to a company to acquire their stakes in it. A company’s contributed capital includes the value paid for equity ...

What is the par value of a stock?

of a stock is usually a small amount (e.g., $0.10 or $0.01) that appears on stock certificates. In some cases, the par value can even be lower than $0.01. The par value must not be confused with the market value of shares. Par value indicates the minimum value at which a company may sell its shares to investors.

What is the difference between a shareholder and a stakeholder?

Generally, a shareholder is a stakeholder of the company while a stakeholder is not necessarily a shareholder.

What is secondary market?

Secondary Market The secondary market is where investors buy and sell securities from other investors. Examples: New York Stock Exchange (NYSE), London Stock Exchange (LSE). do not affect the company’s paid-in capital since it does not receive any cash for the transactions.

What Are Small Stock Dividends?

The treatment of small stock dividends differs from the treatment of splits effected as dividends. This is because they serve fundamentally different purposes.

Large Versus Small Stock Dividends

Up to this point, the discussion has focused on small stock dividends, which range from 20% to 25%. Occasionally, a corporation will issue a large stock dividend. The accounting profession defines a large stock dividend as one in excess of 20% to 25%.

Identifying Small and Large Stock Dividends

Accountants must be able to identify whether a particular stock dividend is small or large.

Example: How to Pay Small Stock Dividends

This example shows a disclosure from Checker Motors Corporation related to the declaration and payment of a small stock dividend.

What Is Additional Paid-In Capital (Apic)?

- Additional paid-in capital (APIC) is an accounting term referring to money an investor pays above and beyond the par valueprice of a stock. Often referred to as "contributed capital in excess of par,” APIC occurs when an investor buys newly-issued shares directly from a company during its initial public offering (IPO) stage. APIC, which is itemized...

How Additional Paid-In Capital (APIC) Works

- During its IPO, a firm is entitled to set any price for its stock that it sees fit. Meanwhile, investors may elect to pay any amount above this declared par value of a share price, which generates the APIC. Let us assume that during its IPO phase the XYZ Widget Company issues one million shares of stock, with a par value of $1 per share, and that investors bid on shares for $2, $4, and $10 ab…

Special Considerations

- APIC is generally booked in the SE section of the balance sheet. When a company issues stock, there are two entries that take place in the equity section: common stock and APIC. The total cash generated by the IPO is recorded as a debit in the equity section, and the common stock and APIC are recorded as credits. The APIC formula is:

Additional Paid-In Capital vs. Paid-In Capital

- Paid-in capital, or contributed capital, is the full amount of cash or other assets that shareholders have given a company in exchange for stock. Paid-in capital includes the par value of both common and preferred stockplus any amount paid in excess. Additional paid-in capital, as the name implies, includes onlythe amount paid in excess of the par value of stock issued during a c…

Benefits of Additional Paid-In Capital

- For common stock, paid-in capital consists of a stock's par value and APIC, the latter of which may provide a substantial portion of a company's equity capital, before retained earningsbegin to accumulate. This capital provides a layer of defense against potential losses, in the event that retained earnings begin to show a deficit. Another huge advantage for a company issuing share…