As a general rule of thumb, subtract your age from the number 110 in order to determine your target stock allocation. For example, if you're 35, this rule says that approximately 75% of your assets should be in stocks.

What is the best asset allocation of stocks and bonds by age?

It is the best asset allocation of stocks and bonds by age for most people in my opinion. The formula simply takes 120 minus an investor’s age to calculate the stock allocation percentage e.g. 120 – 40 year old = 80% in stocks. I use 120 because we live longer. The “New Life Model” is the base case asset allocation for the general public.

Should the percentage of bonds in your portfolio equal your age?

This financial axiom states that the percentage of bonds in your portfolio should equal your age, based on the notion that as we move nearer to retirement, we want to replace the growth potential and risk of stocks with the relative predictability of bonds. For example, if you are 25, 25% of the value of your portfolio should be in bonds.

How much should you allocate to stocks and bonds?

The proper asset allocation of stocks and bonds generally follows the conventional model. The classic recommendation for asset allocation is to subtract your age from 100 to find out how much you should allocate towards stocks. The basic premise is that we become risk averse as we age given we have less of an ability to generate income.

What is the correct asset allocation by age?

To start, there is no “correct” asset allocation by age. But there is an optimal asset allocation I’d like to share in this post. Your asset allocation between stocks and bonds depends on your risk tolerance.

What should my bond allocation be?

The rule of thumb advisors have traditionally urged investors to use, in terms of the percentage of stocks an investor should have in their portfolio; this equation suggests, for example, that a 30-year-old would hold 70% in stocks, 30% in bonds, while a 60-year-old would have 40% in stocks, 60% in bonds.

How should I invest at 35?

5 Tips for Investing in Your 30sStart with your 401(k) Your 20-something self was right about the 401(k) part: That's the first place most people should save for retirement. ... Supplement with a Roth IRA. ... Take as much risk as you can stomach. ... Seek inexpensive diversification. ... Take off the retirement blinders.

Do I need bonds in my portfolio in my 30s?

Although most folks in their 30s are better off putting the bulk of their money into stocks, it pays to invest a small portion of your portfolio in bonds. But don't tie up too much of your money in long-term, low-yield investments, because if you do, you could wind up falling short in retirement.

Is 70/30 A good asset allocation?

One of the simplest strategies for setting asset allocation is to use a percentage split, such as 70/30 or 80/20. Either one has you investing the majority of your money in stocks with the rest going to safer investments, such as cash and bonds.

Is 35 too old to start investing?

Key Takeaways. It's never too late to start saving money for your retirement. Starting at age 35 means you have 30 years to save for retirement, which will have a substantial compounding effect, particularly in tax-sheltered retirement vehicles.

How much money should a 35 year old have?

So, to answer the question, we believe having one to one-and-a-half times your income saved for retirement by age 35 is a reasonable target. It's an attainable goal for someone who starts saving at age 25. For example, a 35-year-old earning $60,000 would be on track if she's saved about $60,000 to $90,000.

Where should I invest in my 30s?

Investments to consider in 30sEquities. ... Public Provident Fund. ... Other fixed-income schemes. ... Insurance. ... Assess income and expenditures to plan for retirement and other goals. ... Building a strong and lasting portfolio. ... Be a stickler for financial discipline. ... Use schemes based on the power of compounding.More items...•

How can I invest in my 30s to be rich in my 40s?

0:412:08:12How To INVEST In Your 30's To Be WEALTHY In Your 40's | Lewis HowesYouTubeStart of suggested clipEnd of suggested clipFirst calculate how many days weeks months or. Years. You can live on your saving. Because when youMoreFirst calculate how many days weeks months or. Years. You can live on your saving. Because when you do that you'll start to you'll gain. Security you'll gain that okay.

What should my portfolio look like at 30?

The old rule of thumb used to be that you should subtract your age from 100 - and that's the percentage of your portfolio that you should keep in stocks. For example, if you're 30, you should keep 70% of your portfolio in stocks. If you're 70, you should keep 30% of your portfolio in stocks.

What is a 80/20 portfolio?

In investing, the 80-20 rule generally holds that 20% of the holdings in a portfolio are responsible for 80% of the portfolio's growth. On the flip side, 20% of a portfolio's holdings could be responsible for 80% of its losses.

What is the average return on a 75 25 portfolio?

Even using 75/25 bumps you up to a little over 5 percent, less than half the historical rate. With bonds doing 2 percent, allocating 75 percent of your portfolio to stocks, they would need to do 14 percent a year to achieve the 10.7 percent average annual return that a 60/40 portfolio delivered.

What is the average return on a 60/40 portfolio?

The rallies of recent years were a boon to 60/40 portfolios, with rock-bottom interest rates pushing up both bond prices and stock valuations, particularly those of high growth companies. The mix delivered an average return of 18% from 2019 through 2021, according to data compiled by Bloomberg.

Why is it important to allocate stocks and bonds by age?

The Proper Asset Allocation Of Stocks And Bonds By Age. The proper asset allocation of stocks and bonds by age is important to achieve financial freedom. If you allocate too much to stocks the year before you want to retire and the stock market collapses, then you’re screwed.

How to build wealth and have the proper asset allocation?

The best ways to build wealth and have the proper asset allocation is to get a handle on your finances by signing up with Personal Capital. They are a free online platform which aggregates all your financial accounts on their Dashboard so you can see where you can optimize.

What is the Financial Samurai model?

The Financial Samurai model is a hybrid between the Nothing-To-Lose model and the New Life model. I believe stocks will outperform bonds over the long run, but we’ll see continued volatility over our lifetimes. I also believe this is the most proper asset allocation if you consistently read my site.

What is survival asset allocation?

The Survival Asset Allocation model is for those who are risk averse. The 50/50 asset allocation increases the chances your overall portfolio will outperform during a stock market collapse because your bonds will be increasing in value as investors flee towards safety.

What happens if you allocate too much to stocks?

If you allocate too much to stocks the year before you want to retire and the stock market collapses, then you’re screwed. If you allocate too much to bonds over your career, you might not be able to build enough capital to retire at all. Just know the proper asset allocation is different for everyone. There is no “correct” asset allocation ...

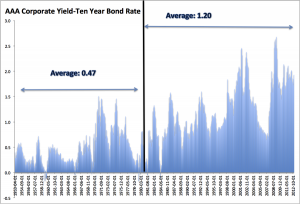

Is the 10-year bond yield inversely correlated?

Bonds and interest rate performance is inversely correlated. Since July 1, 1981, the 10-year bond yield has essentially been going down thanks to technology, information efficiency, and globalization. As a result, the 10-year bond has performed well during this same time period.

Is the S&P 500 volatile?

The S&P 500 has been volatile over the past 20 years. The golden age was between 1995-1999. 2000-2002 saw three years of double digit declines followed by four years of gains until the economic crisis. 2020 was another banner year in the stock market, closing up 18%. So far, 2021 is having a banner year.

Final Word

So which retirement asset allocation strategy is best for you? This decision would be a whole lot easier if we had a crystal ball.

Additional Resources

Before joining project finance as a writer, Mike worked in the active trading division of such firms as thinkorswim, TD Ameritrade and Charles Schwab. His work has appeared in the Financial Times, the Chicago Sun-Times, and The Buffalo News. Contact: [email protected]

What are the three main asset classes?

The three main classes are stocks/equities, fixed income, and cash or cash equivalents. Outside of those, in the context of portfolio diversification, people usually consider gold/metals and REITs to be their own classes too. Let’s look at why asset allocation is important.

What is asset allocation?

Asset allocation refers to how different asset classes are proportioned in an investment portfolio, and is determined by one’s investing objectives, time horizon, and risk tolerance. Asset allocation is extremely important, more so than security selection, and explains most of a portfolio’s returns and volatility.

Why are stocks and bonds held together?

For example, stocks and bonds are held alongside one another because they are usually negatively correlated, meaning when stocks go down, bonds tend to go up, and vice versa. That uncorrelation between assets offers a diversification benefit that helps lower overall portfolio volatility and risk.

Why are stocks more risky than bonds?

Buying stocks is a bet on the future earnings of companies. Bonds are a contractual obligation for a set payment to the bond holder. Because future corporate earnings – and what the company does with those earnings – are outside the control of the investor, stocks inherently possess greater risk – and thus greater potential reward – than bonds.

Why is asset allocation important?

Asset allocation is an extremely important foundation for one’s investment portfolio. It is dependent on the investor’s time horizon, goals, and risk tolerance. There are several simple formulas that can be used in helping determine asset allocation by age. Take the time to assess all these factors for yourself.

How old can a woman live under the 100 rule?

However, many investors believe certain factors mean The 100 Rule needs a bit of tweaking. For example, people are living longer — especially women. In fact, the Social Security Administration recently reported that the average 65-year-old woman can expect to live up to age 86.6.

Is it wise to invest your money based on your age?

Setting an asset allocation based on your age is a smart way to start planning for your retirement or building wealth. But there is no one-size-fits-all strategy. Generally speaking, most investors believe you should invest more of your money in growth-oriented equities like stocks when you’re younger.

What happens when the common stock is 55%?

Benjamin Graham explained, “When changes in the market level have raised the common-stock component to say, 55%, the balance would be restored by a sale of one-eleventh of the stock portfolio and the transfer of the proceeds to bonds. Conversely, a fall in the common-stock proportion to 45% would call for the use of one-eleventh of the bond fund to buy additional equities.” 1

What is 15/50 stock rule?

A 15/50 Stock Rule portfolio requires more risk tolerance than one based on your age, especially if you are in your 70s. Higher risk is assumed if you build your portfolio to a 50/50 split and then leave it to grow; however, this split comes with a risk-mitigation tactic—proportional adjustment at 5% in either direction, which maintains the symmetrical value of each of the investment types.

Does the balance provide tax?

The Balance does not provide tax, investment, or financial services or advice. The information is being presented without consideration of the investment objectives, risk tolerance, or financial circumstances of any specific investor and might not be suitable for all investors.

Is interest rate trend hard to predict?

Interest rate trends are famously hard to predict in the short term, but we could be in for a longer period of slowly rising rates. That means the high annual return that bonds have averaged since 1976 would be unlikely, with yields slowly lowering. Consider today’s long lifespans.