Tax Reporting for Qualifying Dispositions of ESPP Shares

- Calculate compensation income. Your compensation income from ESPP shares in a qualifying disposition is the lesser of two amounts. ...

- Check your W-2. The compensation income from a qualifying disposition may be reflected on Form W-2 received from the company maintaining the plan.

- Report your compensation income. ...

- Calculate your basis. ...

How do I report Employee stock purchase plan on taxes?

Jan 21, 2022 · Situation 1: Disqualifying disposition resulting in short-term capital gain. Subtract the actual price paid from the market price at the exercise date. Multiply the result by the number of shares: ($25 - $21.25) x 100 = $375.

What are employee stock purchase plans?

Subtract the amount paid for the stock (option price). The ordinary income might be more than the gain on the sale. The stock’s basis is the total of both: Ordinary income amount; Stock’s option price; Report the amount of ordinary gain as wages on Form 1040, Line 7. Losses on the sale of ESPP stock are capital losses.

Is employee stock purchase plan (ESPP) income taxable?

Find the original stock purchase price, which is also known as the basis, on your 1099. Now check Box A on Form 8949, as the transaction was reported to …

How are employee contributions used to purchase stock?

Depending on the employer’s stock plan, you may elect to pay taxes on the income at the time the stock is awarded, at the time the stock vests, or at the vest date. The amount reported to you as income on Form W-2 by your employer at the time the stock vests will then be your adjusted cost basis in these stock units. Incentive Stock Options (ISO)

Do you pay taxes on employee stock purchase plan?

Do you have to report ESPP on my tax return?

Is ESPP income included in W-2?

Do employee stock options count as income?

What do I do with my employee stock purchase plan?

How do you avoid double tax on ESPP?

How do I report stock plan transactions supplement?

How do I report employee stock options on tax return?

How do I enter ESPP on Turbotax?

How are stock options reported on w2?

It appears on the W-2 with other income in: Box 1: Wages, tips, and other compensation. Box 3: Social Security wages (up to the income ceiling)Jan 22, 2019

How are employee stock grants taxed?

How long do you have to hold stock to sell?

When you sell the stock, the income can be either ordinary or capital gain. The sale will qualify for capital gain treatment as long as the stock is held for both of these: 1 At least two years after the option is granted 2 At least one year after you buy the stock

What happens if you don't meet the holding period requirement?

If you don’t meet the holding period requirement, it’s a disqualifying disposition. You can only recognize ordinary income. To figure the ordinary income amount: Determine the FMV of the stock on the date you received it (exercise date). Subtract the amount paid for the stock (option price).

How long do you have to be employed to exercise an option?

Also, you must stay employed by the company until at least three months before you exercise the option. If you meet the holding-period requirements, your ordinary income from the sale depends on the option price. The option price: Might be less than the fair market value (FMV) of the stock on the date you received it.

How long do you have to hold ESPP shares?

Employees can sell their shares at any time, but they must meet two IRS conditions to retain the favorable tax treatment: The shares must be held for at least two years after enrolling in the ESPP, and they must be held for at least one year after the purchase date.

What is an ESPP?

An Internal Revenue Service-approved employee stock purchase plan, or ESPP, provides favorable tax treatment to employees when they buy and sell company stock.

Where is Karen Rogers?

Based in St. Petersburg, Fla., Karen Rogers covers the financial markets for several online publications. She received a bachelor's degree in business administration from the University of South Florida. Related Articles. How to Handle Restricted Stock 1099-B on a Tax Return.

Do you have to report stock options on your tax return?

However, the Internal Revenue Service (IRS) still requires you to report those benefits on your tax return.

What is restricted stock unit?

Restricted Stock Units (RSU) These stock units are awarded to an employee as a form of compensation. The employee does not receive the stock at the time of the award, but has a specific vesting plan outlining when the employee will receive the stock. At the time the stock vests, the employee receives the units and the fair market value (FMV) ...

How long do you have to hold ISO stock?

The requirements for ISO units are stricter and in turn provide more favorable tax treatment. ISO units must be held for at least one year after the options are exercised. In addition, you cannot sell the shares until at least two years after the options are awarded to you.

Is a discount on a W-2 considered ordinary income?

Based upon how long the employee holds the stock, the discount is considered ordinary income and included on Form W-2 by the employer (nonqualifying position) or it is considered capital gain income and accounted for at the time of sale (qualifying position). For non-qualifying positions, your adjusted cost basis is the compensation income reported ...

When do you get a 1099B?

You will receive a Form 1099-B in the year you sell the stock units. The form reports any capital gain or loss resulting from the transaction on your tax return.

What is Form 3921?

Form 3921 is issued for incentive stock options in the year they are transferred to the employee. It includes the necessary information to properly report the sale of these units when you decide to do so. Save this form with your investment records.

What is a 3922?

Form 3922 is issued for employee stock options that you purchased but do not sell. Since you have not sold the stock, the holding period requirements have not been determined. Therefore, the employer does not include compensation income on your Form W-2 as ordinary income. Form 3922 is issued to report the income on your tax return ...

How much can you contribute to an ESPP?

Under an ESPP program, employees can elect to defer salary and bonus up to the IRS limit of $25,000 per year (the “ Contribution Limit” ). You elect how much to contribute per pay period during an initial “ Enrollment Period”. At the end of this enrollment period, typically every six months, this money is used to purchase shares at a discount ...

What is an ESPP?

Offered by most publicly traded companies, an ESPP is an employee benefit that allows you to purchase shares of your company stock at a discount. It’s this discount that’s the most significant advantage of Employee Stock Purchase Plans. For most employers, you can expect that discount to range between 5%-15%—obviously the higher the better for you! ...

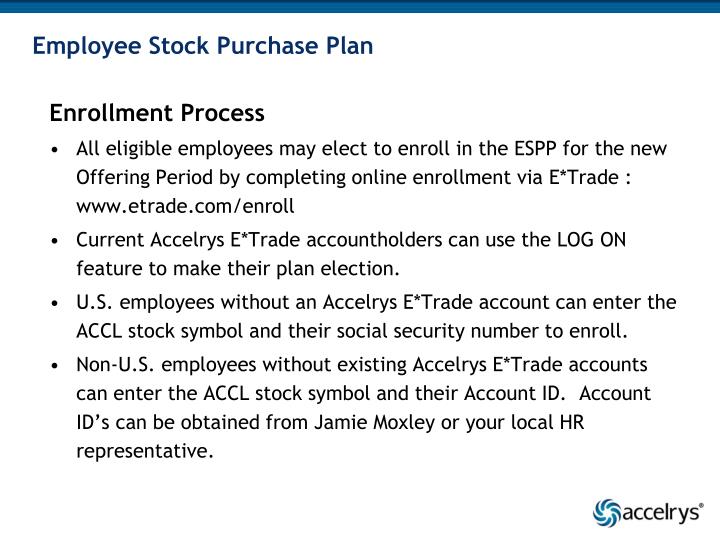

How often does an ESPP enroll?

Typically, every six months your ESPP will have an enrollment period. You’ll elect to participate in the plan and select how much to contribute each pay period. Your contributions into the plan will be directly pulled from payroll at each pay period and accumulate in your ESPP account.

What is the advantage of an ESPP?

As mentioned above, the primary advantage to exploit in an ESPP is the discount. Shares can be sold immediately (known as a “Quick Sale”) and assuming a 15% discount, lock in a minimum 18% pre-tax gain on your money.

What is an ESPP plan?

Summary. An employee stock purchase plan (ESPP) is an organizational-wide stock plan that is offered to employees who meet specific requirements. There are two main types of plans – qualified and non-qualified plans. In order to enroll in an ESPP, it is beneficial to first educate yourself on eligibility, deduction, and taxation.

What is a qualified plan?

Qualified Plans. For an organizational-run qualified plan to be implemented, they must receive the approval of shareholders. Shareholder A shareholder can be a person, company, or organization that holds stock (s) in a given company.

What is defined contribution plan?

Defined-Contribution Plan A defined-contribution plan (also known as a DC plan) is a type of pension fund payment plan to which an employee, and sometimes an employer, Employee Retention.

What is an ESPP?

What is an Employee Stock Purchase Plan (ESPP)? An employee stock purchase plan (ESPP) refers to a stock program that allows participating employees to purchase their organization’s stock at a discounted price. In some cases, organizations offer stock discounts as high as 15%. Rather than directly purchasing their organization’s stock, ...

What is the enrollment period?

Enrollment Period: The enrollment period is the period of time where you can choose to either enroll or deny entry into the purchase plan. Offering Date: The offering date is the period when payroll deductions begin. Offering Period: The offering period is an extension of the offering date.

What is employee morale?

Employee Morale Employee morale is defined as the overall satisfaction, outlook, and feelings of well-being that an employee holds in the workplace. In other. , loyalty, and retention. Participants get a sense of organizational pride. If the company succeeds, so do the employees.

Do you have to report capital gains on stock?

1 Additionally, when shares are sold, you’ll need to report the capital gain or loss. Learn more about taxes, when they’re paid, and how to file your tax return.

Does Fidelity provide tax forms?

Fidelity provides you the tax forms you’ll need based on what you did with your stock during the prior year. Be sure to wait until you receive all your forms and documents before you file.

What is cost basis?

Cost basis is just a fancy term given to the purchase price paid to acquire shares —and it’s used to determine the gain or loss when those shares are sold. For stock plans, your cost basis may need to be adjusted to reflect the compensation income you already reported and paid tax on.

Statutory Stock Options

If your employer grants you a statutory stock option, you generally don't include any amount in your gross income when you receive or exercise the option. However, you may be subject to alternative minimum tax in the year you exercise an ISO. For more information, refer to the Instructions for Form 6251.

Nonstatutory Stock Options

If your employer grants you a nonstatutory stock option, the amount of income to include and the time to include it depends on whether the fair market value of the option can be readily determined.

Preliminary explanation

These rules impose reporting requirements on a disposition of ESPP shares that occurs after you have held the shares long enough to avoid a disqualifying disposition.

What you need

Income from a qualifying disposition of ESPP stock may or may not appear on Form W-2, so that is one item you need. If you sold the shares (instead of making a different kind of disposition, such as a gift), you should also have Form 1099-B, which reports your proceeds from the sale.

Step 1: Calculate compensation income

Your compensation income from ESPP shares in a qualifying disposition is the lesser of two amounts.

Step 2: Check your W-2

The compensation income from a qualifying disposition may be reflected on Form W-2 received from the company maintaining the plan. That doesn’t always happen, so you should check your W-2. It may be difficult to isolate this amount because it is not listed separately.

Step 3: Report your compensation income

If the compensation income from your qualifying disposition was included in the wages reported on Form W-2, simply report the number from your W-2 on your tax return the way you normally do. If it was not included on your W-2, add the ESPP compensation to the wages on your Form W-2 and report the total as wages on your tax return.

Step 4: Calculate your basis

Next you need to calculate your basis for the shares. This is the amount you paid for the shares, increased by the amount of compensation income reported. If your qualifying disposition was a gift, you should provide this basis information to the recipient of the gift. If the disposition was a sale, proceed to Step 5.

Step 5: Report the sale of the shares

Report the sale of the shares on Schedule D, using the sales proceeds reported on Form 1099-B and the basis calculated in Step 4. You had to hold the shares more than a year (and perhaps longer) to have a qualifying disposition, so your gain or loss is long-term.