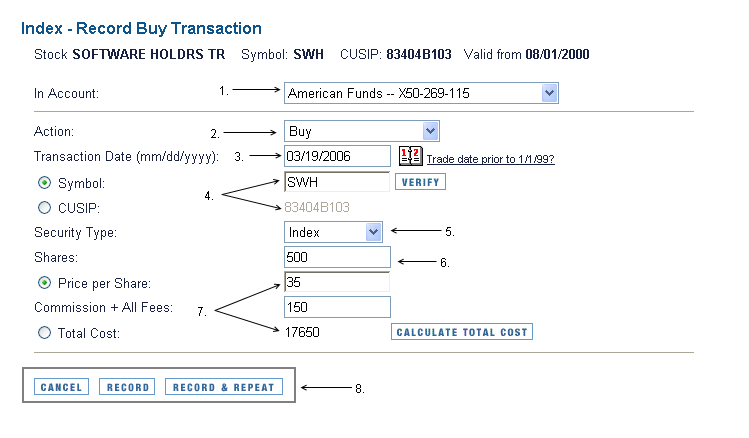

How do I record a corporate acquisition (stock-for-stock)?

- Open the account you want to use.

- Click Enter Transactions.

- In the Enter Transaction list, select Corporate Acquisition (stock for stock).

- Use this dialog to change the security name and price information when a corporation acquires another corporation or entity you currently own and ...

- Company acquired.

- Acquiring company.

- New shares issued.

- Price per share for acquiring company.

- Memo.

- Click Enter/New to enter another transaction, or Enter/Done t o finish.

How do you record stock purchases in accounting?

To record the stock purchase, the accountant debits Investment In Company and credits Cash. At the end of each period, the accountant evaluates the value of the investment. If the value declined, the accountant records an entry debiting Impairment of Investment in Company and credits Investment in Company.

How does an accountant record an asset purchase?

At the end of each period, the accountant evaluates the value of the investment. If the value declined, the accountant records an entry debiting Impairment of Investment in Company and credits Investment in Company. The accountant records the asset purchase by debiting Asset and crediting Cash or Note Payable.

How to do the acquisition purchase accounting process?

The Acquisition Purchase Accounting Process. 1 Identify a business combination. 2 Identify the acquirer. 3 Measure the cost of the transaction. 4 Allocate the cost of a business combination to the identifiable net assets acquired and goodwill. 5 Account for goodwill.

What is a purchase and sale record?

Every purchase record indicates the date and cost. Each sale accounts for a date and proceeds received. When matching each sale to a prior purchase, the oldest owned shares of a specific stock are typically considered sold first.

What is the journal entry for a stock purchase?

The company can make the journal entry for purchase of stock investment by debiting the stock investments account and crediting the cash account. Stock investments account is an asset account on the balance sheet, in which its normal balance is on the debit side.

Which method should be used to record the acquisition?

Purchase acquisition accounting is now the standard way to record the purchase of a company on the balance sheet of the acquiring company. The assets of the acquired company are recorded as assets of the acquirer at fair market value. This method of accounting increases the fair market value of the acquiring company.

Where do acquisitions go on the balance sheet?

Acquisition cost is placed on a company's balance sheet under the fixed assets section. The total cost included on the balance sheet will include all costs incurred to use the asset, including costs associated with getting the asset working and producing.

What are the steps in accounting for an acquisition?

Steps in Acquisition Method of Merger AccountingStep 1: Identify the Acquirer. ... Step 2: Determining the Acquisition Date. ... Step 3: Recognising & Measuring Identifiable Assets Acquired & Liabilities. ... Step 4: Recognising and Measuring Any Non-Controlling Interest (NCI)More items...

Which method should be used to record the acquisition of a fixed asset?

The cost method involves recording the acquisition cost of the fixed asset, plus the costs of bringing the fixed asset to the condition and location required for its use.

What is the difference between equity method and acquisition method?

The equity method and the acquisition method report the same net income. However, assets and liabilities are highest under the acquisition method and lowest under the equity method. It implies that ROA will be higher under the equity method (smaller denominator) relative to the acquisition method).

Are acquisition costs capitalized or expensed?

Transaction costs are capitalized In an acquisition of a business, transaction costs are expensed on, or prior to, the acquisition date. In an asset acquisition, transaction costs are a cost of acquiring the assets, and therefore initially capitalized and then subsequently depreciated.

Is an acquisition an expense?

The cost of acquisition is the total expense incurred by a business in acquiring a new client or purchasing an asset. An accountant will list a company's cost of acquisition as the total after any discounts are added and any closing costs are deducted.

What is the difference between purchase and acquisition?

Acquire = "buy or obtain (an object or asset) for oneself." Purchase = "acquire (something) by paying for it; buy."

Where do acquisitions go on the income statement?

Under standard accounting rules, any costs you incurred to carry out the acquisition are considered part of the purchase price, according to Corporate Finance Institute. As such, they go on the balance sheet as capitalized costs, not on the income statement as expenses.

How are accounts payable handled in an acquisition?

The purchase price paid to the owner is reduced by the amount of accounts payable that is being assumed by the buyer. Then the buyer, as the new owner, pays the invoices as they become due.

Where do acquisitions go on the cash flow statement?

In conclusion, “Acquisitions, Net of Cash Acquired” measures the net amount of cash a company spent to acquire other companies. It usually appears on the Cash Flow Statement under Cash Flow from Investing as a negative number.

Why is proper accounting of stock important?

The Lenders and the management as well need to analyze the financial position of an entity before taking any decision, the proper accounting of stock helps in analyzing the amount which the company has raised by way of stock issuance.

What is goodwill valuation?

When someone wants to take over the business, then for the valuation of goodwill#N#Valuation Of Goodwill Goodwill valuation is the systematic evaluation of the goodwill of the company to be shown in the balance of the company under the head intangible assets and top methods to value include Average Profits Method, Capitalization Method, weighted average profit method and the Super Profits Method. read more#N#or capital reserve#N#Capital Reserve Capital reserve is a reserve that is formed from the company's profits earned from its non-operating activities during a period of time and is retained for the purpose of financing the company's long-term projects or writing off its capital expenses in the future. read more#N#, one needs to analyze the stock accounts as the permission of stockholders is required.

What is stock accounting?

Stock Accounting refers to recording the transaction entered into by the business enterprise from the point of investments made by anyone i.e. whether a body corporate or individual in the company in exchange of issue of something in return which could be easily traded in the open market.

What is a stock certificate?

Stock Certificate Stock Certificate, also called a Share Certificate, is a legal document evidencing the ownership of stocks in a Company, including details like the stockholder’s name, issuing date, the total number of stocks issued, identification number, and the corporate seal & sign. read more. is known as Stock Accounting.

What is capital reserve?

Capital Reserve Capital reserve is a reserve that is formed from the company's profits earned from its non-operating activities during a period of time and is retained for the purpose of financing the company's long-term projects or writing off its capital expenses in the future. read more.

What is treasury stock?

Treasury stock is the stock that the company repurchases its own shares back from the market. Likewise, the company needs to record the purchase of treasury stock as a contra account to stockholders’ equity on the balance sheet. As the treasury stock is a contra account to the stockholders’ equity, the purchase of treasury stock will reduce both ...

What is cost method in stock?

Under the cost method, the company can simply debit the treasury stock account at the amount paid for the purchase. The company usually records the purchase of the treasury stocks first before deciding whether to resell them or retire them later.

Can a company record a purchase of treasury stock?

The company can record the purchase of treasury stock with the journal entry of debiting the treasury stock account and crediting the cash account. In this journal entry, the par value or stated value of the stock, as well as the original issued price, is not included with recording the purchase of the treasury stock.

Does treasury stock affect the legal capital?

However, the purchase of treasury stock does not affect the legal capital (i.e. paid-in capital) of the company. This is due to the number ...

Can a company record a stock purchase without a debit?

However, it is useful to note that when the company purchases the treasury stocks with the intention to retire them immediately, it may directly record the purchase and retirement of the stock without the need to record the debit of the treasury stock. Such journal entry for the recording of the purchase ...

Does journal entry affect legal capital?

This journal entry does not affect the legal capital of the company as the treasury stock is separately presented on the balance sheet as a contra account to the stockholders’ equity and the number of issued shares of the company is still the same.

What happens to treasury stock when it is sold above its cost?

If the treasury stock is sold above its cost, the sale increases (debits) cash for the proceeds received, decreases (credits) treasury stock for the cost paid when the treasury stock was repurchased , and increases (credits) additional paid‐in‐capital—treasury stock for the difference between the selling price and the repurchase price.

Why do companies buy treasury stock?

Companies purchase treasury stock if shares are needed for employee compensation plans or to acquire another company, and to reduce the number of outstanding shares because the stock is considered a good buy. Purchasing treasury stock may stimulate trading, and without changing net income, will increase earnings per share. ...

What happens if the stock's market value is not yet determined?

If the stock's market value is not yet determined (as would occur when a company is just starting), the fair market value of the assets or services received is used to value the transaction. If the total value exceeds the par or stated value of the stock issued, the value in excess of the par or stated value is added to ...

What is the cost principle of stock?

If corporations issue stock in exchange for assets or as payment for services rendered, a value must be assigned using the cost principle. The cost of an asset received in exchange for a corporation's stock is the market value of the stock issued. If the stock's market value is not yet determined (as would occur when a company is just starting), ...

Does purchasing treasury stock increase earnings?

Purchasing treasury stock may stimulate trading, and without changing net income, will increase earnings per share. The cost method of accounting for treasury stock records the amount paid to repurchase stock as an increase (debit) to treasury stock and a decrease (credit) to cash. The treasury stock account is a contra account to ...

Is a corporation's stock considered an asset?

As a corporation cannot be its own shareholder, any shares purchased by the corporation are not considered assets of the corporation. Assuming the corporation plans to re‐issue the shares in the future, the shares are held in treasury and reported as a reduction in stockholders' equity in the balance sheet.

What is journal entry for stock investment?

The company can make the journal entry for purchase of stock investment by debiting the stock investments account and crediting the cash account. Stock investments account is an asset account on the balance sheet, in which its normal balance is on the debit side.

What is stock investment account?

Stock investments account is an asset account on the balance sheet, in which its normal balance is on the debit side. Likewise, in this journal entry, there is no impact on the total assets of the balance sheet as it results in the increase of one asset (stock investment) and the decrease of another asset (cash).

Why do companies need to make journal entries for stock purchases?

Likewise, the company needs to make the journal entry for the purchase of stock investment when it decides to purchase it as an investment asset. Purchase of stock investment provides two main benefits to the company, in which the first one is that it can earn the dividend revenue from the investment. And another one is that it can enjoy the ...

Is journal entry for stock purchase similar to debt investment?

It is useful to note that even though the journal entry for the purchase of stock investment is similar to the purchase of debt investments, it may be different from one investment to another when it comes to the recognition of revenue and dividend from the stock investments. This will depend on how much ownership the company has in other companies.

Why do we need to record common stock transactions?

Maintaining a record of common stock transactions is required for investors to measure their performance and report the results for income tax. A stock transaction is recorded when shares are purchased and when they are sold.

Do shares have a basis?

However, shares given to you have a basis of either the fair market value when received or the basis of the previous owner. If you receive additional shares as a stock dividend, allocate your cost basis in the initially acquired stock among the new shares and those previously owned.

Is a holding period of more than one year long term?

A holding period of more than one year is recorded as “long term.”. Ownership for one year or less is “short term.”. This will simplify quick identification of tax treatment without referring to the purchase and sale dates.

What is an acquiree's identifiable assets and liabilities?

Acquiree’s identifiable assets and liabilities. Subject to the recognition criteria, the acquirer recognizes separately, as part of allocating the cost of the combination, only the identifiable assets, liabilities, and contingent liabilities of the acquiree that existed at the acquisition date.

What is acquisition date?

Any costs directly attributable to the business combination. The acquisition date is the date on which the acquirer effectively obtains control of the acquiree.

What is a private entity?

In actuality, the private entity is the acquirer if it has the power to govern the financial and operating policies of the legal parent.

What are the types of assets that an acquirer should allocate at the acquisition date?

Types of Assets Common types of assets include current, non-current, physical, intangible, operating, and non-operating. Correctly identifying and.

When should acquirers recognize liabilities?

This is only recognized when the acquiree has, at the acquisition date, an existing liability for restructuring in its accounts.

What is IFRS N?

Under IFRS#N#IFRS Standards IFRS standards are International Financial Reporting Standards (IFRS) that consist of a set of accounting rules that determine how transactions and other accounting events are required to be reported in financial statements. They are designed to maintain credibility and transparency in the financial world#N#, the expenditure during the research part of an in-process research and development (IPRD) project must be expensed. However, subsequent expenditures during the development phase of a project (the commercial development of existing research knowledge) may be capitalized post-acquisition. Under US GAAP, neither past expenditure on research nor on development is treated as a separable asset acquired as part of the acquisition.

What does "separable" mean in accounting?

Is separable (traceable); or. Arises from contractual or other legal rights. For identifiability, separability, as well as contractual and legal rights, are taken into account. Accounting principles aim to reflect that an entity’s equity value is reflected in the value of its intangible assets.

How does an accountant record a stock purchase?

The accountant records each purchase through a journal entry. To record the stock purchase, the accountant debits Investment In Company and credits Cash. At the end of each period, the accountant evaluates the value of the investment.

How do companies use their cash?

These companies use their cash for different purposes, including purchasing stock in other companies or purchasing assets to use in the business. When a company purchases stock, it evaluates various companies to find the right stock. It also evaluates the potential risk of each investment and the financial outlay required. When a company purchases an asset, it evaluates the equipment’s ability to meet the company’s needs. Several differences exist in the accounting for stock purchases and asset purchases.

What is the difference between asset and stock purchase?

Asset purchases represent a business investment.

Do stock purchases require cash?

Stock purchases generally require the company to pay cash for these assets. In this case, the company needs to use excess cash or borrow cash from a lender in order to make the purchase. Asset purchases present financing options in addition to cash purchases. The accountant evaluates the cost of financing the asset. 00:00.

Is a stock purchase a financial investment?

Financial Investment. Stock purchases and asset purchases both represent investments for the company. The company accountant analyzes the costs and benefits of each investment before the company confirms the purchase. A stock purchase represents a financial investment.

Explanation

- A stock acquisition includes everything on the balance sheet, both assets and liabilities. If the buyer needs a tax write-off, this may be a viable option. A stock sale involves buying the entire entity, so past financial and legal liabilities are included, creating significant exposure for the buy…

Types of Stock Accounting

Stock Accounting Entries

How to Record Stock?

- Stock is of two types. One is the inventories which we hold to be traded or being utilized for some other produced finished goods. The other is shares, also known as stock. In this article, we are...

- Every business needs funds to operate its business effectively. So to manage such funds, some business chooses the option of issuing stocks in the open market. They raise funds by …

- Stock is of two types. One is the inventories which we hold to be traded or being utilized for some other produced finished goods. The other is shares, also known as stock. In this article, we are...

- Every business needs funds to operate its business effectively. So to manage such funds, some business chooses the option of issuing stocks in the open market. They raise funds by way of allotment...

- After that, the process of recording the transaction of receiving the money from the public at large and issuing them the stock certificateStock CertificateStock Certificate, also called a Share Ce...

Benefits

- The company issues stocks against cash. I.e., cash will be received by the company, and the investor will receive a stock certificate.

- In this option, stocks were issued for consideration, which is other than cash. i.e., issuing stock for taking some services, etc.

- The last type is issuing stock for purchasing some existing stock issued in the market. In oth…

- The company issues stocks against cash. I.e., cash will be received by the company, and the investor will receive a stock certificate.

- In this option, stocks were issued for consideration, which is other than cash. i.e., issuing stock for taking some services, etc.

- The last type is issuing stock for purchasing some existing stock issued in the market. In other words, to repurchase the stock issued earlier new stock is going to be an issue.

Conclusion

- As discussed above, there are three types of stock for which we have to pass the recording entries, which are as follows: #1 – Where Stocks are Issued for Cash In the case where stocks are issued for cash, then to record the transaction following two entries need to be journalized in the books of accounts: *In a case where the stock is issued at a ...

Recommended Articles

- Let us understand the recording of stock with an example, company A wants to issue stock amounting to $100,000 comprises of 10,000 stock of $10 each on 01.04.2020 and to issue stock certificates to the applicants on 10.04.2020, then to record such transaction in the books of accounts following entries are to be passed: On date 01.04.2020: Then on date 10.04.2020, to al…