How do you find the variance of a stock return?

- Find the initial cost of the investment.

- Find total amount of dividends or interest paid during investment period.

- Find the closing sales price of the investment.

- Add sum of dividends and/or interest to the closing price.

- Divide this number by the initial investment cost and subtract 1.

Is variance good or bad for stock investors?

In the Sales row, the variance amount is a positive value and is a good variance because we would like our Sales income to be greater than our Budgeted income. In the Cost of Sales row the variance amount is shown as a positive value but it is actually a bad variance because we would prefer our expenses to be less than what was budgeted.

How does the expected return affect a stock price?

Key Points

- A company that is publicly traded must announce its earnings reports quarterly. ...

- Beta is a metric used to signal the risk in a particular stock. ...

- Analysts constantly assess the health of public companies to assess the value of its equity and debt instruments, and their outlook affects stock and bond prices in secondary markets.

How do you calculate expected return on a stock?

Expected return is calculated by multiplying potential outcomes (returns) by the chances of each outcome occurring, and then calculating the sum of those results (as shown below). In the short term, the return on an investment can be considered a random variable. Random Walk Theory The Random Walk Theory is a mathematical model of the stock market.

How to calculate stock's realized annual return?

How to calculate an annual return Here's how to do it correctly:

- Look up the current price and your purchase price.

- If the stock has undergone any splits, make sure the purchase price is adjusted for splits. If it isn't, you can adjust it yourself. ...

- Calculate your simple return percentage:

How do you calculate stock return variance?

Let's start with a translation in English: The variance of historical returns is equal to the sum of squared deviations of returns from the average ( R ) divided by the number of observations ( n ) minus 1.

What is the variance of return?

In the portfolio theory, the variance of return is called the measure of risk inherent in a singular or in an asset of portfolios. In general, the higher the value of variance, the bigger is the squared deviation of return of the given portfolio from the expected rate.

How do you find the variance of a stock in Excel?

Sample variance formula in ExcelFind the mean by using the AVERAGE function: =AVERAGE(B2:B7) ... Subtract the average from each number in the sample: ... Square each difference and put the results to column D, beginning in D2: ... Add up the squared differences and divide the result by the number of items in the sample minus 1:

What is the variance in stocks?

Variance is a measurement of the spread between numbers in a data set. Investors use variance to see how much risk an investment carries and whether it will be profitable. Variance is also used to compare the relative performance of each asset in a portfolio to achieve the best asset allocation.

How do I calculate the variance?

Steps for calculating the varianceStep 1: Find the mean. To find the mean, add up all the scores, then divide them by the number of scores. ... Step 2: Find each score's deviation from the mean. ... Step 3: Square each deviation from the mean. ... Step 4: Find the sum of squares. ... Step 5: Divide the sum of squares by n – 1 or N.

How do you find the variance of a single stock?

1:073:29Variance of a Single Asset - YouTubeYouTubeStart of suggested clipEnd of suggested clipSo that's the sample variance or s squared is equal to the sum of the variance column divided by theMoreSo that's the sample variance or s squared is equal to the sum of the variance column divided by the total number of sample readings. Minus one which gives you a larger.

How do you calculate the VaR of a portfolio in Excel?

Finding VaR in ExcelImport relevant historical financial data into Excel. ... Calculate the daily rate of change for the price of the security. ... Calculate the mean of the historical returns from Step 2. ... Calculate the standard deviation of the historical returns compared to the mean determined in Step 3.More items...

What is standard deviation of stock returns?

Standard deviation is the statistical measure of market volatility, measuring how widely prices are dispersed from the average price. If prices trade in a narrow trading range, the standard deviation will return a low value that indicates low volatility.

How do you find the variance and standard deviation of a stock?

The formula for the SD requires a few steps:First, take the square of the difference between each data point and the sample mean, finding the sum of those values.Next, divide that sum by the sample size minus one, which is the variance.Finally, take the square root of the variance to get the SD.

What is Variance?

Variance is a metric that is needed to estimate the squared deviation of any random variable from the mean value. In the portfolio theory, the variance of return is called the measure of risk inherent in a singular or in an asset of portfolios.

Formula: How to Calculate Variance

We have two different approaches to calculate the variance of returns −

Probability Approach

The probability approach for determining variance is used when the complete set of possible outcomes is available. This means the probability distribution of the asset or portfolio is known in advance.

Historical Return Approach

The historical return approach is more generally used in investing and finance. Using finite data set of the history of the investment in an asset or a portfolio, the return is calculated with assumptions that each possible outcome has the same probability. Thus, the variance of return on a single asset or portfolio is measured as −

Favorable vs. Unfavorable Variance

As variance analysis is done for both revenues and expenses, it’s crucial to carefully distinguish between the two sides of impacts – the positive or negative impact. For this reason, the terms favorable and unfavorable are used instead of saying positive, negative, over or under, etc., as they make the point clearer.

Variance in Budgeting and Forecasting

The variance formula is very useful in budgeting and forecasting. It gives a clear picture when analyzing results. It helps the financial analyst to perform his duties appropriately and with utmost accuracy.

Step 1

Subtract the price at the start of the year from the price at the end of the year to find the raw increase in stock price. For example, if the stock started at $26 and ended the year at $29, the stock increased by $3.

Step 2

Divide the increase or decrease by the price at the start of the year. In this example, divide the $3 increase by the $26 starting price to find that the stock increased by 0.1154, or about 11.54 percent.

Step 3

Repeat steps 1 and 2 to calculate the return on the stock for each year. For example, if you wanted to know the variance over the past three years, you would calculate the returns for each of those years.

Step 4

Calculate the average return on the stock by adding the annual return and dividing the result by the number of years. In this example, if the stock increased by 11.54 percent in the first year, increased by 5.46 percent in the second year, and lost 2 percent in the third year, add 11.54 plus 5.46 minus 2 to get 15 percent.

Step 5

Calculate the difference between the average return and each annual return. In this example, the difference between 0.1154 and 0.05 is 0.0654 percent; the difference between 0.0546 and 0.05 is 0.0046, and the difference between minus 0.02 and 0.05 percent is 0.07.

What is the effect of a higher variance on a stock?

A stock with a higher variance can generate returns that are much higher or lower than expected, which increases uncertainty and increases the risk of losing money. You can calculate variance and returns using a stock’s historical price information.

What is historical variance?

A stock’s historical variance measures the difference between the stock’s returns for different periods and its average return. A stock with a lower variance typically generates returns that are closer to its average.

What is standard deviation in investment theory?

Standard Deviation From a statistics standpoint, the standard deviation of a data set is a measure of the magnitude of deviations between values ...

What is correlation in statistics?

Correlation A correlation is a statistical measure of the relationship between two variables. The measure is best used in variables that demonstrate a linear relationship between each other. The fit of the data can be visually represented in a scatterplot. Negative Correlation.

How many stocks does Fred own?

Fred holds an investment portfolio that consists of three stocks: stock A, stock B, and stock C. Note that Fred owns only one share of each stock. Information about each stock is given in the table below:

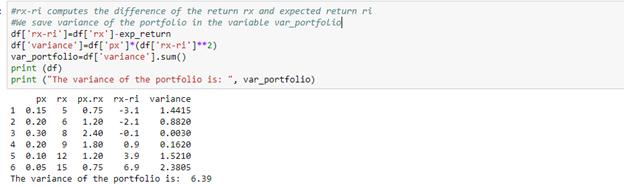

How to calculate portfolio variance?

To calculate the portfolio variance of securities in a portfolio, multiply the squared weight of each security by the corresponding variance of the security and add two multiplied by the weighted average of the securities multiplied by the covariance between the securities.

How can portfolio variance be reduced?

Modern portfolio theory (MPT) states that portfolio variance can be reduced by selecting securities with low or negative correlations in which to invest, such as stocks and bonds.

How can risk be lowered in a portfolio?

Measuring Risk. Following MPT, risk can be lowered in a portfolio by investing in non-correlated assets. That is, an investment that might be considered risky on its own can actually lower the overall risk of a portfolio because it tends to rise when other investments fall.

What is standard deviation?

Standard deviation is a key measure of risk used by portfolio managers, financial advisors, and institutional investors. Asset managers routinely include standard deviation in their performance reports.

Standard Deviation of a Portfolio

The standard deviation of a portfolio of assets, or portfolio risk, is NOT simply the sum of the underlying securities’ risk. Due to the correlation between securities, the computation of the portfolio risk must incorporate this correlation relationship.

Computing Standard Deviation of Portfolio

For a portfolio with two underlying assets, X and Y, we can compute the portfolio variance as follows: