How much is a voting discount for nonvoting stock?

Prior Tax Court cases whereby the issue of a voting premium or nonvoting discount was highlighted can also provide some insight. As indicated in the adjacent table, the courts generally have allowed discounts ranging from 0% to 5% for nonvoting stock, consistent with the market studies previously discussed.

What is the valuation discount for the lack of voting rights?

the valuation discount for the lack of voting rights is typically not as large. The application of a discount to reflect the differ - ence in value between a share of stock that has the right to vote and a share of stock that does not have such a right is encountered with some regularity by valuation analysts.

Why do minority interests in voting and nonvoting stocks differ in valuation?

Each valuation exercise has a unique set of facts and circumstances. The key factors contributing to greater price differentials between minority interests in voting and nonvoting stock lie in the ability to influence greater shareholder returns and the likelihood that these events will materialize.

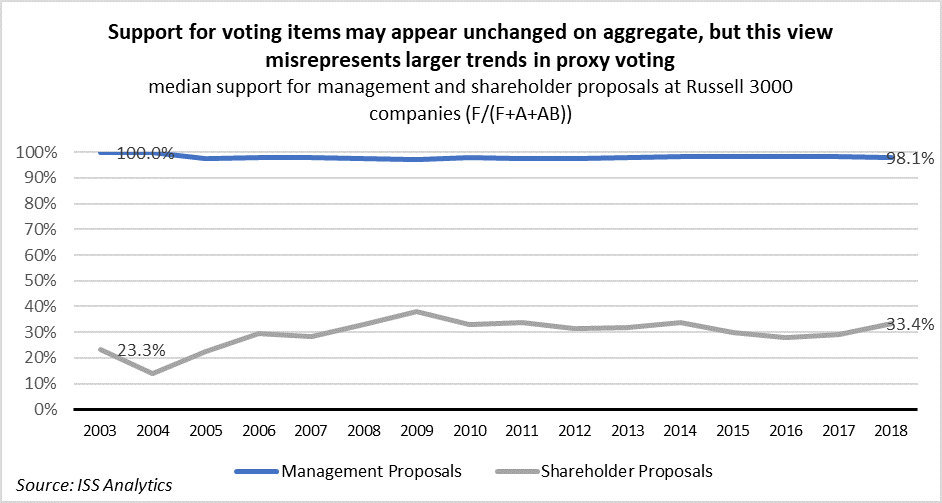

Do shareholders extract a price discount for lack of voting privileges?

The empirical data also indicates that shareholders will extract a price discount for the lack of voting privileges related to the common shares of a public corporation.

Are voting shares worth more than non-voting?

Each voting share is worth five percent more per share than each nonvoting share.

Why would investors buy stock with no voting rights?

Non-voting shares are offered when the directors or founders of a company want to raise new share capital without losing their control of the company. They do this by offering large numbers of non-voting shares, which the public can buy to own a stake in the company.

How much stock do you need to have voting rights?

Thus, somebody owning more than 50% of a company's shares can effect a majority of the vote and is said to have a controlling interest in the firm.

What is the difference between voting and nonvoting shares?

Voting shares enable the shareholders to vote on certain corporate matters such as electing the board of directors (who oversee the management of the corporation). Non-voting shares do not allow the shareholders to vote on certain corporate matters.

Are non-voting shares worth less?

Typically, non-voting shares are priced between 0-5% less than voting shares – so it's not a big difference in cost to the investor initially, however, if you are also giving up dividend payouts that is something to consider whether it's worth investing in even if the stock price was slightly cheaper.

Are non-voting shares worth less than voting shares?

Since the impact associated with control is minimal in efficiently managed companies, voting shares and nonvoting shares should trade at approximately the same price.

What happens if a shareholder does not vote?

Broker Vote For certain routine matters to be voted upon at shareholder meetings, if you don't vote by proxy or at the meeting in person, brokers may vote on your behalf at their discretion. These votes may also be called uninstructed or discretionary broker votes.

What is non-voting ordinary shares?

Non-voting ordinary shares usually carry no right to vote and no right to attend general meetings. These shares are usually given to employees so that remuneration can be paid as dividends for the purposes of tax efficiency for both parties.

What are the instances that non-voting shareholders are allowed to vote?

The VC requires preferred shares to be issued on the financing. In this case, non-voting shareholders vote with voting shareholders to approve/reject the creation of this superior class of preferred shares to be issued to the VC. You may get the votes.

Do non-voting shares have ownership?

Many companies have an ownership structure that includes both voting shares and non-voting shares. Technically voting shares control the company and non-voting shares do not.

What is super voting stock?

We define super voting common stock as having either (1) a greater number of votes per share than the voting common stock or (2) the ability to elect a disproportionately high number of board of directors members. Therefore, this class of stock has greater-than-normal voting rights in a corporation that has at least two classes of common stock outstanding. Also, we define non-voting common stock as having no voting rights per share. Therefore, this class of stock has less-than-normal voting rights in a corporation that has at least two classes of common stock outstanding.

Is supernormal voting a common occurrence in bankruptcy?

The valuation of equity securities without voting rights or with supernormal ( i.e., superior) voting rights is a common occurrence in a bankruptcy environment. This is true with regard to a debt restructuring where creditors may wind up as nonvoting or supervoting shareholders.

Why did Doss not breach the shareholders agreement?

Doss argued that he did not breach when he left in 1994 because the company never even offered to buy his shares. Accordingly, his obligation to sell was not triggered.

Who owns the stock in Wallace v. Wallace?

In Wallace v. Wallace, three brothers, Phillip, Gary, and Doss collectively owned all of the issued stock in a successful family business passed down to them by their father.

Why is the stock split not likely to be effectuated?

However, the stock split and creation of the new class of nonvoting stock is not likely to be effectuated until later in the year due to shareholder lawsuits seeking to block the move.

Is a minority shareholder disadvantaged?

Moreover, the minority shareholders in that public company may not be disadvantaged in any respect relative to a controlling buyer since minority shareholders generally have equal access to information, have certain legal protections, and are equal beneficiaries of the cash flows (relative to their ownership interest).

Should voting shares be traded at the same price?

All else held constant, voting shares should trade at a greater premium to nonvo ting shares at poorly managed companies relative to optimally managed companies. Since the impact associated with control is minimal in efficiently managed companies, voting shares and nonvoting shares should trade at approximately the same price.

Discount for Lack of Voting Rights (Stock) - Explained

What is a Discount for Lack of Voting Rights? How Does a Discount for Lack of Voting Rights Work? Discount for Lack of Voting Rights

What is a Discount for Lack of Voting Rights?

It is a fixed amount or percentage deducted for the selling price of a block of shares that lacks voting rights.

Why is there a minority discount on stock?

Every share an employee, son or daughter buys, as long as they own less than 50%, is arguably subject to a minority discount for lack of control and for lack of liquidity.

What is minority interest?

A minority interest is non-controlling ownership, usually defined as less than 50% of a company's voting shares. A minority discount is a reduction in the price of stock from its fair market value because the minority interest owner (s) cannot direct or control the business operations, and because of lack of marketability of the stock.

What is non voting stock?

Non-voting common stock is a public corporation stock whose owner does not have voting rights at the annual general meeting of the company.3 min read. 1.

What is the price difference between voting and non-voting stocks?

Several studies have found that the price differential between voting and non-voting stocks is extremely minimal, with most reporting a price differential of only 3-5 percent. This creates a highly lopsided advantage for holders of voting shares.

What are the multiple adjustments required when estimating the value of non-voting stock in a company?

These adjustments include: Discount for lack of control. Discount for lack of marketability. Discount for lack of voting rights.

What are noncontrolling, nonmarketable ownership interests in closely held companies?

These issues often arise during gift tax, estate tax, generation-skipping transfer tax, income tax, property tax and other taxation disputes. To assist valuators in the field, the Internal Revenue Service (IRS) offers some guidance, particularly around two related issues that further cloud analysis: Discount for Lack of Liquidity (DLOL) and Discount for Lack of Control (DLOC).

What is the difference between restricted stock and common stock?

The restricted stock method purports that the only difference between a company's common stock and its restricted stock is the lack of marketability of the restricted stock. Subsequently, the price difference between both units should arise due to this lack of marketability.

What is a DLOM?

Discounts for lack of marketability (DLOM) refer to the method used to help calculate the value of closely held and restricted shares. The theory behind DLOM is that a valuation discount exists between a stock that is publicly traded and thus has a market, and the market for privately held stock, which often has little if any marketplace.

How can a minority interest in a company be controlled in the public stock market?

Protection from many risks attendant to holding a minority interest in a business can be controlled in the public stock market by selling the equity holdings, should the holder decide that management actions are elevating his or her risk beyond an acceptable level. This same ability to liquidate (convert into cash) an interest in a privately held company rarely exists. Moreover, due to size and other specific company nuances, as well as a lack of a perfect market mechanism for disposition, risk attendant to a lack of liquidity or of marketability can often be an issue for even a control interest in a privately held enterprise.

Why do we need blockage discount?

The need for a blockage discount usually arises in consideration of supply and demand influences in the publicly traded securities markets. In other words, a transaction offering a substantial block of a single entity’s issued and outstanding shares may create a supply that exceeds current demand. Such an occurrence will generally impair the subject company’s value because of the reduced liquidity associated with the oversupply.

What is a key person discount?

Business valuators would generally consider an additional discount for a company where thin management and a strong company dependency on the efforts of a single individual for future operational and financial success would threaten the company’s long-term viability. Such a discount is generally referred to as a key person discount.

What is an employee stock ownership plan?

An Employee Stock Ownership Plan can present special issues related to discounts and premiums. Specific questions on the applicability and size of minority discounts and control premiums continue to generate commentary and analysis by business valuation practitioners, the Department of Labor and the courts.

What is restricted stock?

Restricted stock (also known as letter stock) is stock of a publicly traded company that is restricted from trading for a specific period of time. It is identical to the publicly traded stock except that it is not freely traded. Although restricted stock cannot be sold in the public markets, it can be sold in private transactions. These transactions usually must be reported to the Securities and Exchange Commission and therefore become public record, allowing a comparison be done of the price of the restricted stock to the publicly traded stock.

What is the issue of lack of marketability?

One of the more controversial issues in the area of discounts for lack of marketability is whether any discount is applied to a control interest in a business enterprise. The issue has frequently been addressed by the United States Tax Court, which affirms the use of such discounts when valuing controlling interests.

What is the counter agreement to the use of a control premium for self-dealing?

The counter agreement to the use of a control premium for self-dealing is the state corporation statutes in the U.S. , whereby the control shareholders have a fiduciary responsibility to the non-control shareholders. As such, unfair transactions can be mediated by intervention of the courts, sometimes by having the minority shares redeemed at fair value.